Adviser Voice CPD Content Articles

CPD: Modern Portfolio Theory and the Rise of Ratios in Portfolio Construction

The advent of MPT brought a great deal of science and formal theory to portfolio construction.

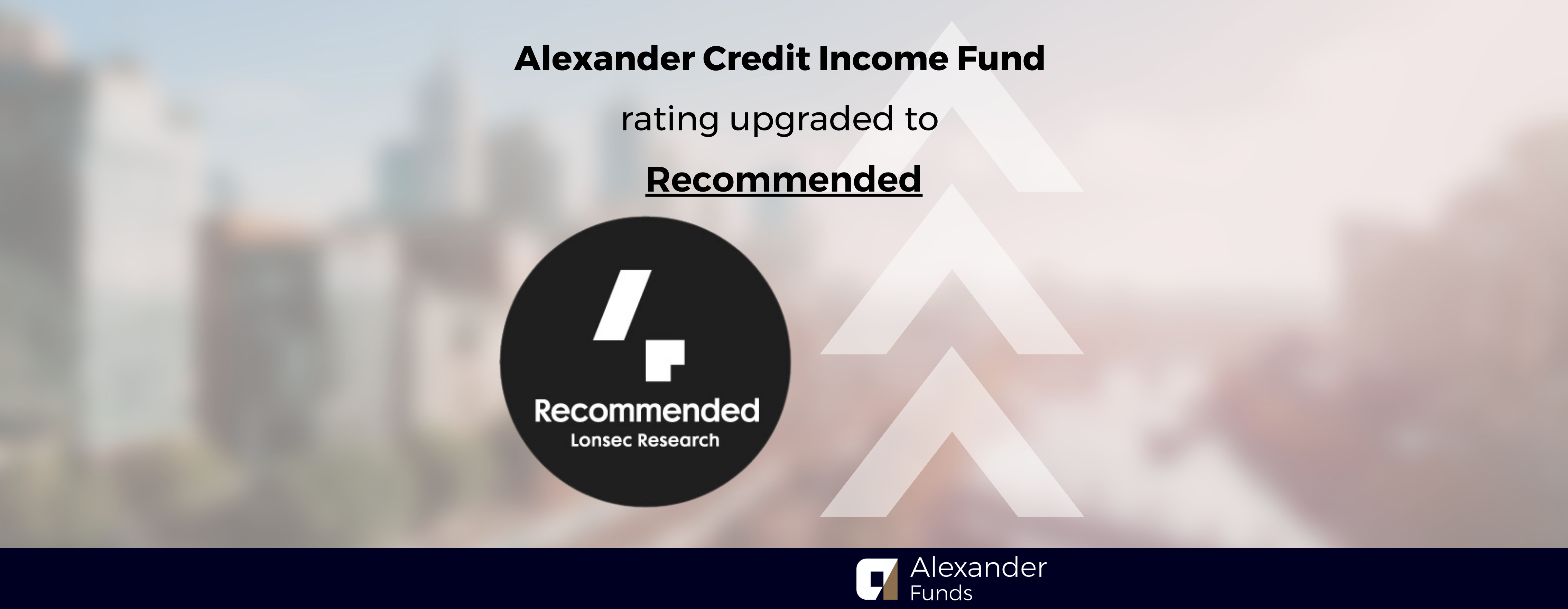

Webinar: Credit Market Update - Readjusting to a higher-rate environment

Click here to access the webinar recording.

With higher interest rates in 2023, it's crucial to...