Introduction

Few financial market topics raise such passion and debate as the Australian housing market.

There are ample points that both support and undermine the argument that the market is overvalued and overdue for a correction. Supporters point to the 2007 collapse of the American housing market, and related investment securities, as a potential scenario domestically. However, there are some major structural differences between these two housing markets that make it hard to compare them directly.

Outside of direct property ownership, investors have exposure to the Australian housing market through various securities, including the extensive Residential Mortgage Back Securities (RMBS) market. Those not overly familiar with the workings of the market may, quickly but erroneously, draw the conclusion that a sustained and significant decline in house prices will cause the market to unravel in the same way that the US market did after their housing collapse. However, the RMBS market has many features that, in the face of falling house prices, still allow investors to benefit from the currently rising yields without exposing themselves to unnecessary risks, including capital losses.

The Australian housing market

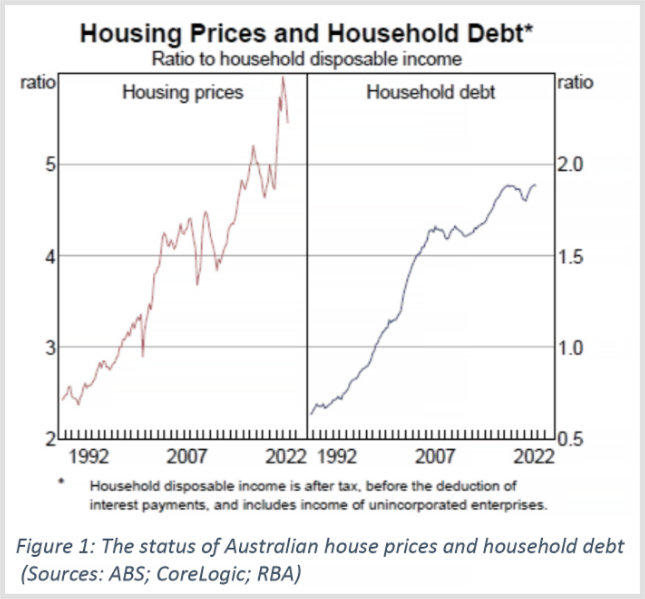

The bear case against the Australian housing market is straightforward, and not without merit. Four graphs are sufficient to provide the necessary insights. Figure 1 shows that after the recession of the early 1990s, Australians have gone on a debt fueled housing binge. With limited new housing supply and favourable tax treatment for residential property investments, house prices have risen to six times the typical household income. As a result, Australia now has one of the most expensive property markets in the world.

As illustrated in Figure 1, the upward trend in house prices has been long standing and has withstood various economic downturns along the way. Throughout this period, many pundits have doubted the sustainability of the Australian housing market and have been surprised by the market’s resilience. Recently, doubts have grown stronger due to the spike up in debt and house prices following various policy responses to the COVID-19 pandemic.

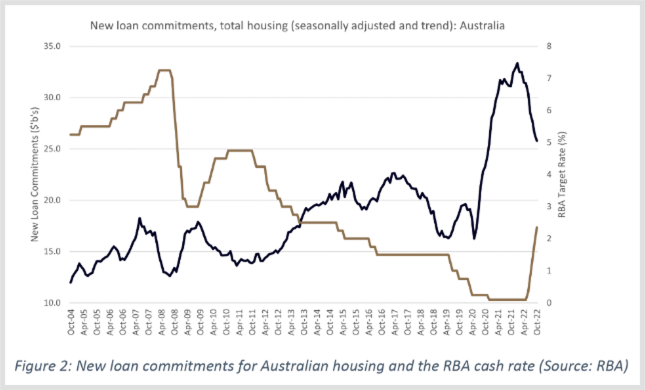

Figure 2 illustrates that once the Reserve Bank of Australia (RBA) started lowering interest rates to stimulate the economy at the onset of the pandemic, Australians rushed out to either buy a new house or add to their housing portfolio. During this period borrowers were able to access very favorable fixed rate loans, which are now resetting at much higher rates.

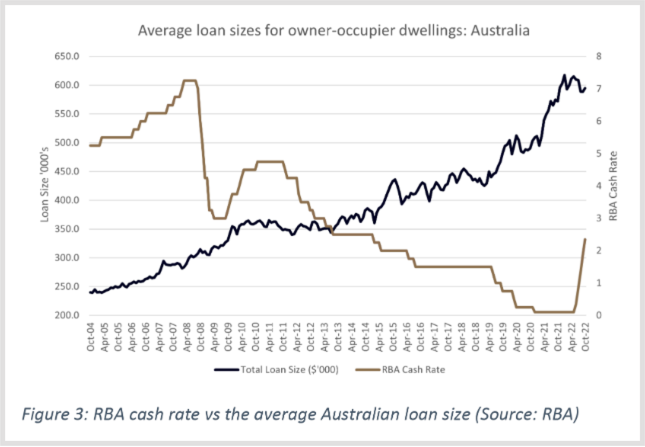

Figure 3 shows that during the recent housing boom Australians were not only willing to take out more loans, but they also wanted larger loans. This willingness to take on more debt, and access to cheap and easy debt, fed a positive feedback loop which saw house price climb up to a point. This point was when the RBA started to rapidly increase interest rates to combat inflation. These rate rises have resulted in an inevitable decline in house prices.

Crucially for the performance of the RMBS market, and in particular conservative investors, the current house price declines are more of a distraction than catastrophe. Section 4 explains how RMBS securities are structured to provide protection from falling prices, and more importantly loan defaults. The latter point is essential, as defaults are the critical variable to the performance of the RMBS market, not just the direction of house prices. Additionally, default levels are negatively affected to a greater degree by high interest rates and rising unemployment, rather than falling house prices.

The Australian RMBS Market

Despite its relative obscurity compared to the equity markets, the Australian RMBS market is material in size and is destined to grow over time. As of November 30, 2022, there was approximately $100 billion of outstanding securities. Of the $100bn 15% are securities issued by major banks, with the remainder coming from non-authorized deposit taking institutions (non-ADI). By the end of 2022 there were at least 12 major non-ADI issuers (an entity that issued more than $1b of securities in 2022), with the leader being Pepper Finance, which issued approximately $5b worth of new securities in the last 12 months.

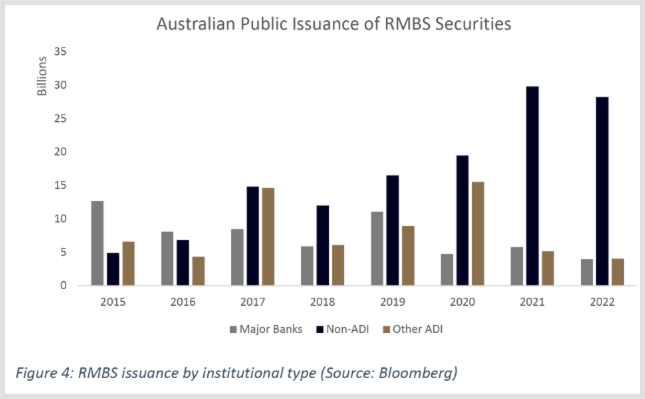

Despite the relatively stable balance of outstanding securities, the RMBS market has a constant supply of new securities being created. This situation occurs because as a debt security, an RMBS has a finite life. An RMBS will typically cease to exist when the issuer “calls” the security after it has amortized to a certain level (although its final legal maturity is the last date any loan within the initial portfolio). At this point the remaining outstanding face value of the security is returned to the holder. The Australian RMBS market has averaged approximately $40 billion of new public issuance over the past five years (see Figure 4), representing a 50% turnover of the market. Additionally, it is estimated that another $10 billion per annual worth of RMBS securities have been issued in private transactions.

Non-ADIs source funds from the RMBS market because they do not have access to customer deposits to fund loans. Like a bank, these lenders make money by exploiting the difference between their lending costs and the rate at which they lend to their customers. Banks also access the RMBS market to recycle capital and improve their capital position by moving loans off their balance sheet through the issuance RMBS securities.

The Australian home loan market has experienced a structural shift, with the non-ADIs growing their presence (see Figure 4) as the major banks have withdrawn from certain segments of the home loan market, for example, self-employed and younger lenders, and higher loan to value ratio (LVR) loans. The banks have been forced into this action due to the higher capital charges they face from regulators for holding loans to these cohorts. This theme will likely see the continued growth of non-ADI lenders.

RMBS Securities

An RMBS is a pool of home loans that have been securitized (combined) by the issuer into a tradeable security(s). RMBS investors receive a monthly coupon, with the holder of the security at maturity also receiving its outstanding face value. The monthly coupon, nominated at issuance, represents the cost of funding for the issuer.

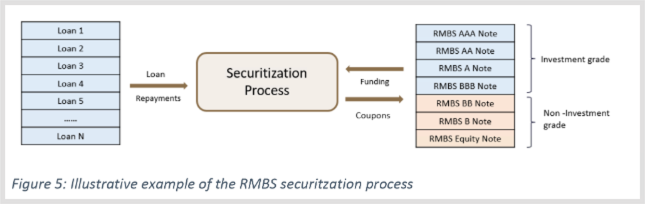

For Australian investors, this coupon is generally floating in nature. The coupon has two components: a base floating benchmark rate, and a fixed spread. As illustrated in Figure 5, the spread varies across the different notes according to the risk of each, with each note connected to the same pool of loans.

By pooling mortgages, the issuer is diversifying the risk of not receiving sufficient loan repayments to pay monthly coupons or returning the required capital at maturity. A shortfall can come about because a mortgage borrower will either fall into arrears with their repayments or completely default. In the instance of default, there is the added risk that the recovered amount from the sale of the property will not cover the outstanding principal of the loan.

Creating tranches in a mortgage pool is a vital function within the RMBS market. Tranches divide the original pool of mortgages into several related securities, called notes. Figure 5 provides an illustrative example. Credit enhancement (CE) is the process by which Notes are differentiated by the level of protection against defaults in the pool they receive. Variation in CE result in each security receiving a different credit rating. These rating come from a third-party rating agency, for example S&P or Moody’s. Investors are compensated with a higher spread for taking greater risk through holding a lower rated note. Crucially, CE builds over the life of a RMBS security, thereby lifting the level of protection against losses as time passes.

The composition of the mortgage pool and the level of CE for each Note make a significant contribution to the rating of any RMBS security. In addition, for a loan to be eligible to enter a pool it will need to meet a host of other criteria often including, an acceptable Loan-to-Value Ratio (LVR), a clean payment arrears record, and property type. In addition, Portfolio Parameters will place rules round which an RMBS pool must comply with, including average LVR, geographic concentration limits and lending to certain borrower segments.

Another risk mitigation characteristic of an RMBS is the life expectancy of a mortgage. While mortgages are taken out for a term of 30 years, on average they are paid out or refinanced within seven years. These prepayments plus regular monthly principal payments feed into the conditional prepayment rate (CPR) – which is effectively the annualized percentage of a mortgage pool’s principal that will be paid off ahead of schedule in each period. CPR captures the fact that the total RMBS pool is repaying principal (amortizing) from Day 1 and effectively reducing the risk of any shortfall in payments for most Note classes (outside of the equity note at the bottom).

Falling property prices

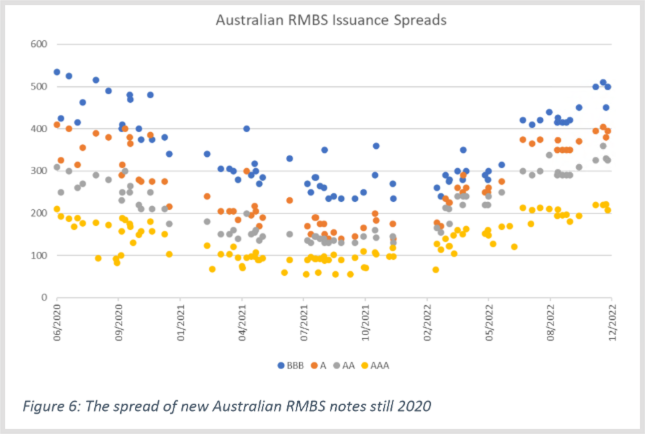

Over the last 12 months, RMBS investors have seen the market reprice in response to rising interest rates and its expected negative effect on growth. Figure 6 shows that the spreads, the proxy for risk, for new issuances have risen to levels last seen at the height of the COVID-19 pandemic. In turn, the spread on existing securities have also pushed out, delivering a mark-to-market loss for RMBS holders.

Despite the deteriorating housing market environment, to this point there has been no noticeable pick up in arrears or defaults within the housing loans underpinning the Australian RMBS market.

If house prices continue to fall what are the feasible outcomes? The best case, which is supported by evidence, is that households have built up significant balances in their offset or savings accounts and will be able to continue to service their loans in the face of rising interest rates. Under this scenario, RMBS spreads are more than likely to stabilize at their current levels.

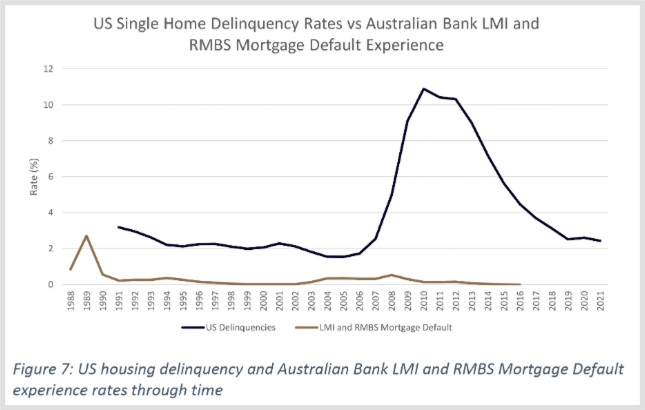

The doomsday expectation is that the RBA lifts rates past the breaking point for many households, resulting in increased defaults in an environment of rapidly falling house prices. Additionally, the tighter monetary policy will lead to higher unemployment, leading to further defaults. If this narrative plays out, how high could defaults go? Figure 7 contrasts the US housing delinquencies rate with the loan impairment rate of Australian financial institutions since 1988. The Australian series is a combination of lender’s mortgage insurance (LMI) claims by the banks and the defaults within RMBS structures. LMI is a significant defensive mechanism utilized by home loan lenders to protect against default losses.

One can see that the Australian market has never experienced loan defaults approaching what the US saw in during the Global Financial Crisis (GFC), including the recession of the early 1990s. As such, the Australian RMBS market has never seen a security default, even at the height of the turbulence in 2008. There are vital differences between the two series which relate to the nature and history of the US home loan market. In the US loans are non-recourse, and there was a substantial volume of sub-prime loans written with predatory practices in the lead up to the GFC. Section 5.1 details the vital differences between the US non-recourse loans and Australian market.

Australian RMBS Market Defenses

Even if defaults pick up in Australia, investors are afforded significant protection through the terms and conditions of Australian home loans. Australian home loans differ in two vital characteristics from the US market. US prime mortgage rates are generally fixed for the life of the loan, while Australian mortgages are predominantly floating, or at best fixed for a small proportion of the loan’s life. The upside of this characteristic for Australian RMBS investors is that interest rate risk is not a consideration, as a note’s market value does not adjust because of changes in interest rates. Therefore, investors can focus their attention on ensuring that their portfolio is receiving sufficient spread to match the prevailing credit conditions and their risk tolerance.

The other difference addresses the rights of a lender to pursue a defaulting borrower for any payment shortfalls. Non-recourse loans, the US situation, means that if a borrower defaults and the lender repossesses the property, any shortfall to the outstanding loan balance from the recovered amounts, after the house is sold, is the full responsibility of the lender. That is the lender has no recourse back to the borrower. If the loan had been securitized, then that loss is passed through to the RMBS security.

Alternatively, loans can be full recourse. Under these conditions if a borrower defaults and there is any shortfall, the lender can pursue the borrower for the shortfall. Therefore, reducing the likelihood of any capital loss, which is minimal in the first instance. The rationale for this last statement comes from the way loans amortize and are prepaid (see Section 4). Regarding the former, a loan may well be written with a LVR of 90%. However, the loan will “season” before it is securitized, thus in effect decreasing the LVR of the loan and increasing the probability of fully recovering any outstanding funds in the face of default. Crucially, homeowners with seasoned loans are likely to have “positive equity” in their house, thereby incentivizing them to protect that equity by not defaulting. Further protecting a RMBS investor is the policy of lenders forcing high LVR borrowers to take out mortgage insurance, which protects the lender in the event of default.

Even if defaults did pick up in Australia, RMBS securities offer significant structural protections for investors. Section 4 outlined these features including CE and the special reserves, which act as a buffer should the mortgages in the pool not generate enough cash to pay out all debt costs in any one month. Critically, CE and these reserves are not static and offer greater and greater protection as a given Note seasons.

Conclusion

The Australian RMBS market has recently seen a material widening in credit spreads in response to rising interests and falling housing prices. These increased spreads ensure that investors are adequately compensated, through higher yields, for the perceived increased risk in the mortgage market. While further widening cannot be ruled out, investors should take comfort that the structural characteristics of RMBS notes offer meaningful capital and income protection in the event of a more severe downturn. Investors also can take further defensive steps by adjusting their own risk exposure via by purchasing RMBS securities with a desirable level of CE.

By Dr Matthew Oldham, Head of Data Analytics